Why the Euro makes no sense

View from the 71st floor of the Raffles Hotel, Shenzhen, China, 2026

A Contemplative Stroll on Hong Kong Island

Recently, on another visit to Hong Kong, walking past the window of a real-estate agent in the fragrant harbour's Wan Chai district, I noticed the HKD24,000,000 (~US$3 million) apartments, the likes of which are available in Budapest for a tenth of the price. It reminded me of a few things, firstly that the geoarbitrage remains the most obvious trade right now, and secondly, of the stories of the 1997 Asian Financial Crisis and its ensuing financial chaos.

In July 1997 the Central Bank of Thailand devalued the baht, triggering massive capital flight, layoffs, bankruptcies and financial pain across the region — what economists describe as a "sudden stop", in which capital flows reverse abruptly and undermine the viability of fixed exchange-rate regimes. Hong Kong's infamously expensive property market, embroiled in the regional panic, collapsed by almost 70%, and reached its nadir in 2003. Underlying structural fragilities had been building for some time. Many regional economies, such as Thailand, Korea, Malaysia and others had seen short-term USD-denominated debt expand rapidly in their private sectors, encouraged by US dollar pegs (or a basket of currencies dominated by the dollar) which made such borrowing attractive, and concealing the risk of maturity mismatches coupled with fixed but unsustainable exchange rates. Companies had revenue denominated in local currency but debt obligations in dollars they could not earn, and by extension, repay.

An economic slowdown was already underway a year earlier in 1996, which began to expose the cracks in the system. Speculators correctly identified the growing current account deficits, mismatched debt obligations, and fundamentally unsustainable dynamics of the Thai baht's peg. They attacked, betting on an inevitable revaluation. Thailand, contrary to the advice of the likes of Singaporeans, exhausted billions of dollars in foreign currency reserves defending the baht, but to no avail [1]. The land of smiles saw its currency fall by around half, the adjustment was swift and brutal, but - unlike Hong Kong -, the adjustment came primarily through the exchange rate, and prices spiked due to higher import costs.

The contagion spread as investors and speculators saw similar structural issues in neighbouring economies. The crisis was underway. Indonesia's rupiah ultimately fell by 80% and Suharto fell the following year - at least in part due to the economic turmoil [1]. The Korean Won and Malaysian Ringgit likewise fell (around 40% against the dollar).

Hong Kong, however, successfully defended its peg of 7.8 Hong Kong Dollars to one American Dollar - a level which still holds to this day. But this didn't mean that Hong Kong was immune to the financial pain, instead the adjustment came through brutal internal revaluations, such as the aforementioned property crash. Economic pain wasn't limited to real estate, rather, the acute internal rebalancing came through higher interest rates, layoffs, downward pressure on wages, rising unemployment and multi-year deflationary pressures.

No economy was immune.

Europe's Illusion of Immunity

Hong Kong's peg resembles a currency union, say that of the Eurozone, in many ways. If the currency of a certain economy - say Greece - cannot adjust, then the wages, real estate and other internal prices must do so instead in order to restore competitiveness and correct internal imbalances.

Real Exchange Rate = Nominal Exchange Rate × (Domestic Price Level / Foreign Price Level)

Because of the inability for Eurozone members to see adjustments in their nominal exchange rates, coupled with the generous and calcified social and taxation system of many of Europe's economies, being a member of the Euro metastasizes as economic suffering for tens of millions of working class Europeans. In effect, member countries of the Eurozone ill-suited to the centralised interest rates and exchange rate level are trapped in a painful economic quagmire unable to adjust their sovereign currency, but also unable to influence interest rates, and therefore beholden to dictats of the ECB and European Commission. At the same time, to exit means complete and utter financial ruin, in the words of Greece's ex-finance minister who held office during the Greek Sovereign debt crisis:

"We [Greece] should not have entered the euro – this is crystal clear, but once in, it is disastrous to remove one's-self from the Eurozone voluntarily" - Yanis Varofakis, Greece's Finance Minister during the European Sovereign Debt Crisis [12]

In early 2026, the incumbent Hungarian government was voted out after 11 years in power. The newly enshrined pro-EU government indicated their intention to join the Eurozone, indicating a desire to follow Bulgaria's footsteps taken a year earlier. Bulgaria, only six months after transitioning to the Euro as the currency unions 21st member, was placed under the EU deficit procedure [6]. A sign perhaps that the system is working, but irrefutable evidence of the abdication of national sovereignty under such an arrangement. Austerity has set Europe back decades when compared to the USA [4], but until recently has remained the economic orthodoxy - driven heavily by German influence - on the continent, no matter the cost.

Bulgaria surrendered the ability to independently monetise its debt and to independently set interest rates, placing those powers within the ECB's common monetary framework. Something the USA, the UK, Japan, Singapore, Australia and the vast majority of developed or semi-developed economies globally retain in their arsenal of economic measures.

Hungary, like Poland, and Czechia, presently retains its own currency. Hungary has, like much of the former Eastern bloc brought into the EU, seen leaps forward in its standards of living, wages, wealth etc since the fall of the Berlin wall. In PPP terms, in 1991, Hungary had a GDP per capita of US$8,352, by 2024 it stood at US$48,552. Poland exceeded this performance and became one of the world's 20 largest economies in 2025 in PPP terms, and now surpasses Spain on a per capita basis (once again, on PPP terms).

It would be intellectually dishonest to make the case that this success has been entirely attributable to their independent, sovereign currencies. Monetary sovereignty has been a contributor, but not the sole factor. As mentioned, Hungary and Poland started from a relatively low economic base in GDP per capita terms - a bad measure but one which gives some context. Poland, Hungary and other former Eastern bloc EU members have been recipients of significant funding from the EU, supercharging their development.

Hungary also suffers from persistent inflation, and the majority of Hungarians in fact support the introduction of the Euro [9]. Stable savings and lower transaction costs, are often cited as reasons to join the common currency.

In reality, a stable currency is within reach for Hungary without joining the Eurozone, and with modern financial solutions and neobanks such as Wise and Revolut, the argument for more efficient transactions is precarious at best - even for businesses subject to cross-border capital flows and revenue streams. However significant the justifications for joining the Eurozone are, it is nevertheless imperative that we consider associated costs. To do this, we need only to cast our eyes West.

Lost Decades

Italy enjoyed decades of strong postwar growth, but since 2000, has stagnated, a reality that is seen in Greece and elsewhere at the Eurozone's "periphery".

Whereas under the Lira, Italy could devalue from time to time to stay competitive, the currency union renders such an approach an impossibility. Italy abdicated its monetary sovereignty at the inception of the Euro in 1999. At the same time, Europe's highly regulated economies - relative to other parts of the world - are averse to violent price change mechanisms such as were witnessed in Hong Kong. Unions, minimum wages, and other frictions within the system mean that the adjustment cannot take place in a reasonable time frame. I am not arguing against these measures, but highlighting economic consequences of them. For example, even in Hong Kong, it took 6 years of deflation and internal price adjustments in the wake of the Asian Financial Crisis, in what is consistently listed as one of the world's freest economies (Hong Kong was ranked the world's no. 1 freest economy in 2023 [3]).

With the lessons of the Asian Financial Crisis in mind, we can better understand the inner workings of the Eurozone quagmire including the sovereign debt crisis. Without a currency to revalue or let float and depreciate, Italy, Greece and the likes saw capital flight within the Eurozone, with capital flight to "safe" Germany and spiking debt yields across economies perceived to be riskier. This suppressed German rates, and spiked costs elsewhere, meaning that the business cycle was accentuated rather than standardised across the currency zone, and that German banks absorbed capital flight from the periphery via the Euro's TARGET2 settlement system.

In Europe, the consequence of a currency union applied to an array of vastly different economies manifests itself as a cost to prosperity. The IMF has reported extensively, along with other research bodies, that economic hardship correlates with lower fertility levels [10]. Undoubtedly, many countries are experiencing ever declining birthrates, but to add economic hardship to the mix is hardly a remedy for this monumental challenge, and has likely exacerbated the trend.

Contrary to common misconceptions, Italians are not lazy, in fact they work more hours per week than those industrious Germans [8]. Italy still boasts massive engineering prowess and world class manufacturers. In fact even in 2026, Italy is Europe's second largest manufacturing economy (excluding Russia).

Once again, the structure of this system prevents interest rates from reflecting conditions of the member economies. Germany's interest rates arguably should have been higher, and yet they have been suppressed to support the weaker economies in Europe. The result - a real-estate bubble and significant malinvestment which has been exposed in the past few years and now contributes to escalating deindustrialisation.

China and the USA

Clearly, the EU seeks to emulate the success of the other two largest economic trade zones: namely China and the USA. They associate scale with power and economic prosperity.

In 1978, when Deng Xiaoping finally rose to power in China, after having been cast out as a "capitalist roader", finally had the chance to implement his reforms of "opening up"[5]. An Optimal Currency Area [7] requires the free flow of labour and capital, fiscal transfer mechanisms (e.g. defense contracts, social security payments in the USA) and similar, synchronised business cycles. Through this lens, Europe's rich tapestry of linguistic, cultural and economic diversity is considered as an economic liability rather than an asset by overpaid Eurocrats in Brussels [11]. Languages and other national idiosyncrasies are a barrier to the free movement of capital, which is why your next business meeting in Europe will likely be in that simplified form of international English we have all come to tolerate (and indeed in Europe unashamedly embrace). By definition, the EU is structurally unable to leverage that which brought Europe to preeminence, while simultaneously hyping the supposed benefits of diversity.

Deng knew from his time in Moscow in the 1920s, where he had studied at the Sun-Yat Sen University, that Lenin's New Economic Policy had injected economic life into the catastrophe of the Bolshevik economy, which lagged well behind pre-revolutionary levels years after the fact [5]. This depressing fact isn't just a number, but one which alludes to the millions who suffered, starved.

Recently, I visited Shenzhen, Deng's first experiment of a free economic zone, for the 3rd time. Today, Shenzhen, is one of China's largest cities and an integral area of the pearl-river delta, with around 86 million people and one of the most prosperous economic zones on the planet. It now exceeds most European cities in terms of safety, technology, development. When you visit Shenzhen, you will see murals and statues of Deng, and be hard pressed to seek out Mao Zedong.

Deng was able to leverage the Optimal Currency Area through free-market Principles under a single currency union because mainland China was not only a single currency union, but also a single political entity.

![note] Imagine for a moment that China, or the USA, could issue a new currency in their poorer regions, to incentivise capital investment, and more accurately reflect the economic conditions of that state or province. Under such a system, Louisiana or Alabama might see better growth and prosperity, as would the Chinese interior, where the coast is much wealthier on average. Such an experiment could equally be considered in the form of a North Euro and South Euro.

But, even without the flexibility of adjustable internal exchange rates, China and the USA have the political will and fiscal mechanisms to direct investment and policies to adjust for regional disparities. The Eurozone as a "monetary union without a political union"[2] lacks this fundamental tool for internal adjustment. From the perspective of EU proponents, this can only be overcome through yet more integration and breaking down of economic barriers between its member states - a principle which can be extended beyond the economic realm to language and culture.

Abolishing the Nations

Under the current paradigm, nation states that form the Eurozone (and the EU more broadly) represent an obstacle to economic prosperity from the perspective of Brussels. Rather than embrace regional currencies that best reflect the economic circumstances of national economies, they seek to further consolidate control and erode the uniqueness of the tapestry of Europe.

This understanding fails to acknowledge the historic realities that smaller economies have generally proven to be more prosperous. Singapore, Hong Kong, Switzerland, Sweden for example which have adapted to crises and emerged as ultra-wealthy societies. Deng was saddled with a gigantic country of a billion people. His policies worked in spite of this because they embraced internal economic freedoms, allowing for policy and price adjustments prohibited under the preceding Maoist rule.

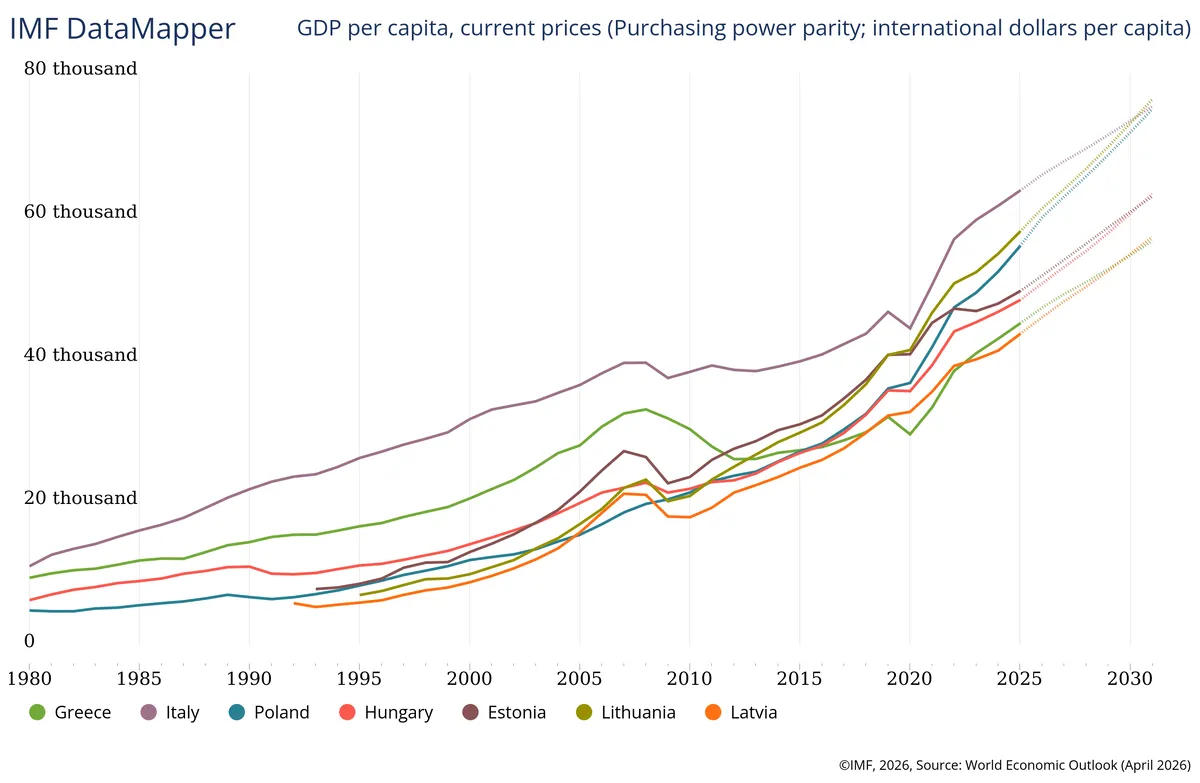

Proponents of the Euro will point to the success of the Baltic club (Latvia, Estonia and Lithuania) which adopted the Euro in 2011.

Chart of Italy, Poland, Hungary, and Baltics showing that growth is comparable, which undermines the authority that a currency union provides prosperity, and at the same time indicates that a sovereign currency is not a prerequisite to success [13].

But the Baltic states are small economies of only a few million people each, which have liberalised their economies massively, in a similar fashion to Shenzhen and the other free-zones within China. Furthermore, their economic prosperity is largely in line with the success of larger EU economies outside of the Eurozone such as Poland (see chart). Adoption of the Euro is not a prerequisite to success, nor is it even necessary. Their success is owed to sound local governance and west-to-east EU fiscal support.

We Saw This Coming After All

In his 1997 piece "The Political Economy of the European Economic and Monetary Union" Martin Feldstein, accurately preempted the ensuing economic malaise, internal division, unemployment and economic underperformance within Europe. All of this is anticipated and was preventable.

Fundamentally, the Euro is not the genesis of Europe's select few success stories, and even proponents would likely acknowledge this, but rather support its adoption as part of a necessary process - which is to say this project is primarily ideologically and politically driven, rather than aiming to prioritise the prosperity of the member states. The single currency has at best had marginal and questionable impact, and at worst, has imposed massive adjustment costs on member states like Italy through removing their monetary flexibility. Even Germany, often touted as a major beneficiary of the Euro, has experienced malinvestments and a distortion of its currency resulting in lower purchasing power and pervasive bubbles in its economy from interest rates that have differed both being too high in the early 2000s, and too low in the last decade.

From plummeting birth rates, malinvestments, chronic underemployment, and an economic malaise that has lasted more than two decades, the Euro has hurt rather than benefited its members. Now with financial technology efficiencies, the already questionable economic benefits even more difficult to quantify. The EU's attempt to overcome this through further consolidation of centralized power erodes the very diversity that made Europe great in the first place. For a technocratic system that prides itself on the "science", that the EU has chosen to ignore such elementary economic realities is palpably ironic.

References

[1] From Third World to First, Lee Kuan Yew, 2000

[2] Adults in the Room: My Battle with Europe's Deep Establishment, Yanis Varofakis, 2017

[3] Fraser Institute, Economic Freedom, 2026

[4] Real Instituto, Elcano - Competitiveness: the widening gap between the EU and the US

[5] From Vladimir Lenin to Vladimir Putin: Russia in Search of Its Identity, 1913–2023, From Vladimir Lenin to Vladimir Putin, 2023

[6] Bulgaria heads for EU deficit procedure months after Euro entry, 2026

[7] Mundell, R. A. (1961). A theory of optimum currency areas. The American Economic Review

[8] Does Germany need to work harder? Its government seems to think so, 2025

[9] Hungary's new government pushes for euro by 2030, 2026

[10] Chart of the Week: Bye Bye Baby—How Crises Affect Fertility Rates - IMF, 2018

[11] 10,000 EU officials better paid than David Cameron, 2014

[12] Interview with J. LUIS MARTIN in OpenDemocracy, 2015

[13] IMF Datamapper, GDP PPP Trends by Country, 2026